The Market Marches Onward and Upward

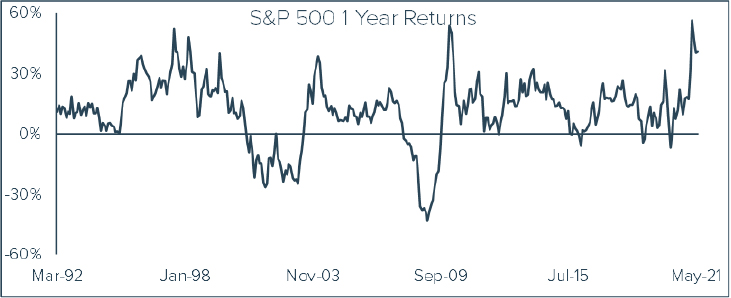

The U.S. stock market continued its relentless move higher. In the previous quarter (March 31, 2021) the S&P 500 Index posted its best 12 month return in more than 30 years (56.35%). This quarter the S&P 500 cooled off only slightly, recording a 40.79% return for the 12 months ended June 30. The 3-year and 5-year returns are not approaching record levels yet, but they are at levels not seen since the market’s recovery from the financial crisis a decade or so ago.

The S&P 500’s annualized 3-year return through June is 18.67%, and the annualized 5-year return is 17.65%. Periods of outsized returns are rarely followed immediately by precipitous declines, but they are often followed by periods of more modest returns. Unusually robust market returns most often come at the expense of future returns, but only time will tell if that is to be the case this time.

Despite volatile bond yields, soaring energy costs, fears of inflation, and supply chain issues that may have derailed less spectacular markets, stocks surged for the 5th consecutive quarter. Growth once again outperformed value, after value enjoyed a brief moment last quarter. Clearly the investing public anticipates the continuation of a very strong recovery.

As the world reopens from COVID, just about everything seems to be in demand. Travel is booming, leisure and hospitality are nearly back to pre-COVID levels, and the consumer is spending. People are ready to get out and enjoy themselves, clearly. About the only sector of the economy that has yet to experience this resurgence is business travel. As long as work-from-home continues to be acceptable for businesses, we believe this sector will continue to be slow to recover. Yet hotels and airplanes seem to be full in spite of the absence of the customers they once valued most.

There are things bubbling below the surface that need not be cause for concern yet, but certainly warrant monitoring. One such thing is the ever-growing presence of investment allocation models sponsored by large investment firms. To be sure, there is nothing inherently disturbing about an investment firm offering advice as to how to allocate your investment portfolio across asset classes. What could be troubling at some point, however, is the degree to which the investing public follows these models. If everyone owns the same thing, it could be difficult to get out or in when changes are recommended. If models ever suggest lessening exposure to stocks, it is not hard to envision a messy decline as everyone rushes to sell in order to stay in line with the model.

This concern was highlighted in a recent Wall Street Journal article by Dawn Lim. She points out that models now control $4.8 Trillion in U.S. fund assets as of March 31st. This is up from $3 Trillion a year prior. That is a lot of money following models. If they all make similar recommendations, all that money will be moving in the same direction. That can be good news when the direction is higher, but could pose a challenge when the direction is lower.

Also worth noting is the persistently low dividend yield. With interest rates near zero, dividend yields have understandably been low for some time now. It is worth noting that, historically, dividends account for approximately 1/3 of market returns. The S&P 500 yields less than 2%, and has for some time. If this continues to be the case, and the contribution of the dividend to total return remains 1/3, then future stock returns will likely be less robust than they are presently. Time will tell how these things play out. For now, the market seems carefree, so enjoy it.

Commentary

Sometimes Analogies are Just Easier to Understand

Imagine that I have successfully persuaded you to manage my money. Specifically, I have convinced you to construct a portfolio for me of residential real estate located exclusively within your home town. You no doubt have a decent understanding of residential real estate, and likely some pretty strong opinions about the local market as well. No matter. You have agreed, and so you proceed.

There is no way for you to easily or immediately replicate the “market”. There is no ETF or fund you can put my money into in order to satisfy my demands. Instead, you must construct this portfolio thoughtfully, one property at a time.

You will employ your own criteria to identify properties worth owning, and you will seek out those that meet your criteria at a price you think reasonable to pay. The day I hand you the money is certainly not the same day all properties will be identified and purchased. This will take time.

If your local real estate market is a buyer’s market, your task might be easier. There will likely be plenty of opportunities to choose among. If, instead, your market favors the seller, you must search more deliberately to find properties for my portfolio. There are always bargains available. Sometimes, it simply requires greater effort and patience to identify them.

The process takes however long it takes. It may even be the case that you don’t spend (invest) all the money, because there just aren’t enough opportunities to use every dollar. And that is okay, because you continue to search for opportunities for the uninvested cash. Maybe you will find an unexpected bargain, and having the extra cash will be a blessing.

After initial construction of the portfolio is complete, the process of actually managing this real estate portfolio begins. Suppose someone offers you 3 times what you just paid for a property. This is obviously more than you consider the property’s fair value. You have been given a gift by an anxious purchaser. Since this is my money (remember), I beg you to accept this gift and sell the property!

Are you selling because you have some other property you want to buy? Or because you have a particular view of the market that informs you to sell? Not at all! You are selling this property because it is the right thing to do.

And now you have more cash. You continue to search for properties that meet your criteria, whatever they may be, at prices you think are reasonable to pay. Suppose that while you are searching, zoning regulations for one of your properties changes and a highway is to be constructed through the back yard. Understandably, this property needs to be sold as well.

Again, are you selling because you have some other property you want to buy, or because you have a particular view of the market that informs you to sell? No. You are selling this property because it is the right thing to do.

With the sale of the second property complete, you have even more cash than before. That is because there have been more properties to sell than there have been to buy. This will eventually change, and when it does, you will be well-positioned to take advantage of opportunities. You avoided the temptation to buy simply because you had cash, so now you have the ability to make the appropriate buys when they present themselves. This is sound management on your part. Congratulations, and thank you for treating my money this way.

For whatever reason, most of us understand real estate and can relate to this analogy. When it comes to stocks, the notion of diligence with patience seems less readily understood or accepted.

Among the investing public, media and other observers, there seems to be some sort of mystique around “the market”. There is great excitement when “the market” goes up, and much hand-wringing when it goes down. And bizarrely, the more the market goes up, the less risk the public perceives. Similarly, during market declines, risk is perceived to be rising.

At Tandem, we take a very different view. We don’t invest simply for the sake of being invested, and the Fund’s portfolio looks quite different from broad market indexes often viewed as “the market”. Much like the real estate analogy, we try to identify those businesses (instead of properties) that meet our criteria at prices we think are reasonable to pay. We are not attempting to replicate “the market”. We are attempting to make sound investments, one at a time.

Unlike with real estate, we can sell some of what we own in a company without having to sell all of it. So when a company the Fund owns is trading at a price we think is unreasonably and unsustainably high, we can take advantage of this gift and sell a piece of our holding, not all of it. Recall in the real estate portfolio someone offered 3 times what we paid for a property, so the property was sold. In the Fund, we can use the same philosophy, yet still own that company, just in a smaller amount.

We typically do not liquidate overvalued companies, but we do reduce our exposure to the risk of an overpriced security. And we do this not because we have another company to buy, or because we have a negative view of the market and want to hold more cash. We do this because it was the right thing to do for a particular company at a particular price.

If a particular company ceases to meet our criteria, we can sell all of our holdings in that company. Whether we have something else to buy is not part of the decision-making process. We sell the company because it is the right thing to do, and we will redeploy the cash when opportunities present themselves, but not before.

When real estate prices rise unrelentingly, most would-be buyers rightly become skeptical. However, when stock prices rise unrelentingly, most want to participate more. If you doubt this, please check the data. Purchases of mutual funds and ETFs historically are greatest at or near market tops. Conversely, sales of mutual funds and ETFs are greatest at or near market bottoms. But in real estate this would be called a buyer’s market!

Why do so many perceive less risk when stock prices are higher and greater risk as prices fall? I can’t say. But at Tandem, we believe that lower prices and higher prices both present opportunities.

Lower prices, in our view, make for more compelling investments than do higher prices. Higher prices are often gifts to be taken advantage of by selling a partial stake, while lower prices are a chance to put that money back to work. This is how to buy low and sell high. Too often investors actually do the reverse – buy when prices are high and sell when prices are low.

Most investors tend to be trend aware. They try to identify the next big thing, or jump into whatever seems to be working now. But eventually trends reverse, and the investor must know when to move on.

Tandem prefers to try to be opportunistic when the market misprices companies. We call this mean-reversion investing. Mean-reversion is about math, not anticipation or guesswork. Rather than hoping to identify the next trend, we rely upon a simple statistical concept based on the notion that most of the time, stocks are fairly valued. And whenever they are not, there is a very high statistical probability that they will revert back to fair value eventually.

In the short term, or sometimes even the medium term, this practice can seemingly put us at odds with the market. And that is okay, because those odds favor a reversion to a more normal valuation eventually.

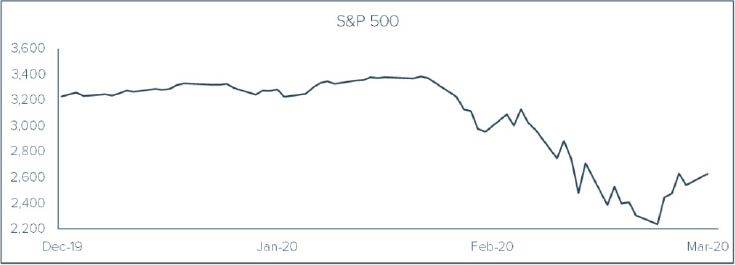

By allowing cash to accumulate when there are more things to sell than buy, we are setting up our portfolio to take advantage of the lower prices that often follow. If you doubt this is so, allow me to remind you of last year. We began 2020 with a relatively high percentage of cash in the Fund. Some questioned this tactic, but we explained this is what buying low and selling high looks like. There just hadn’t been any buying opportunities in a while, so we gave the appearance of just being sellers. Until March of 2020 came and the steep price declines gave us numerous opportunities to put that cash to work. In fact, some of the same people that were concerned about the large amount of cash became concerned when the cash was largely gone! Emotions are a tricky thing, no doubt.

Imagine if we had acquiesced and not followed our discipline. We would not have had all the cash we had accumulated. Two things likely would have happened.

First, the decline to the portfolio would have likely been much more severe. Not because cash stemmed losses, but rather because what we sold to accumulate cash was either overvalued or fundamentally flawed. These types of companies generally perform worse in a market downturn, so we reduced our exposure to them.

The second likely thing to happen would be that we would not have been able to take advantage of the market’s dramatic decline.

When mean reversion is applied to the real estate market, everyone gets it. There are buyer’s markets and seller’s markets. When this discipline is applied to the stock market, it may seem less intuitive, but it is no less effective. Buying low and selling high always makes sense.

A Reminder About Cash as an Asset in the Fund

In a world with interest rates near zero, or even less than zero in some cases, it may be difficult to consider cash an asset. But cash is most certainly an asset, and an important one in the Castle Tandem Fund.

We don’t allocate to cash. We have no view of the market that causes us to increase or decrease the amount of cash in the Fund. The amount of cash is dynamic, not static or targeted. As more opportunities to buy than to sell present themselves, cash levels, by default, decrease. Or, when there are more things to sell than buy, cash levels will rise.

The return on cash is less important to us than the simple availability of cash. Cash doesn’t typically go down in value and is liquid. These features are important. When opportunities present themselves, cash simply has to be available when we need it.

The opinions expressed are those of the Fund’s Sub-Adviser and are not a recommendation for the purchase or sale of any security.

The Standard & Poors 500 Index (S&P 500) is an index of 500 stocks.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund, and it may be obtained by calling 1-877-743-7820 or visiting www.castleim.com. Read it carefully before investing. Distributed by Rafferty Capital Markets, LLC Garden City, NY 11530.

Important Risk Information

The risks associated with the Fund are detailed in the Fund’s Prospectus. Investments in the Fund are subject to common stock risk, sector risk, and investment management risk. The Fund’s focus on large-capitalization companies subjects the Fund to the risks that larger companies may not be able to attain the high growth rates of smaller companies. Because the Fund may invest in companies of any size, its share price could be more volatile than a fund that invests only in large-capitalization companies. Fund holdings and asset allocations are subject to change and are not recommendations to buy or sell any security.

Comments are closed.