Market Comments

In broad strokes, our investment process is based on the principles of being careful and being prepared. We invest when we can identify high quality companies that can be purchased at substantial discounts to our conservative estimate of their intrinsic value. As these obvious bargains are not always present, we are willing to add to the Fund’s cash position and wait patiently for opportunities to appear. A growing cash position is not a market call on our part, it is simply an outcome of our conservative and patient approach to equities. Ultimately we seek to outperform the S&P 500 over a full-market cycle.

To download a PDF of this report, click here.

During market draw downs, having cash on hand may have the dual benefits of 1) acting as a cushion against draw downs, and 2) allowing us to be buyers when others are sellers. Ideally we would like to be more fully invested. However, we are patient value managers and believe that waiting for the right entry price on an investment is a key driver of long-term total returns. Right now we see the price of many operating companies as being very expensive.

Nature can be Indifferent and Unforgiving

Imagine two young hikers setting out for an afternoon hike on a warm spring day. The hikers, wearing shorts and t-shirts, arrive at the base of the peak and park their car. It’s a short hike that they are familiar with, with stretches of open trail, some rock scrambles, and one rather challenging portion near the summit that requires them to negotiate a narrow ledge. The hikers reach the top of the peak late in the afternoon. Shortly thereafter an unexpected storm front quickly moves in and drenches them. The narrow ledge, now wet and slippery, separates them from the trail down to their car. The hikers, not comfortable negotiating the narrow ledge in the rain, wait at the top for the storm to pass. By the time the storm is over the sun has set and the hikers are not confident that they can traverse the ledge in the dark. They feel trapped and decide that their best option is to hunker down and spend the evening on the mountain. The temperature drops quickly that spring evening and the two hikers, in damp clothing, are not prepared to withstand the elements. Our hikers are now in a life-threatening situation.

When the two hikers in our allegory set out on their hike that warm afternoon we doubt that they gave much thought to bringing along a jacket, a tent, a box of matches or even a flashlight. When they embarked on their hike the sun was bright, the air was warm and they simply didn’t think that these items were necessary under these conditions. They were young, strong, confident and unprepared for change. While this allegory highlights the unsympathetic nature of the great outdoors, it also offer an analogous lesson for investors: those who are ill-equipped for changing market conditions may experience unexpected outcomes and dire circumstances. After more than eight years of strong stock market returns, we wonder if many investors may be overly confident and unprepared for the possibility of equity markets to move in the opposite direction.

Let’s rewind the story and imagine the hikers at home preparing for the hike. One of them grabs a flashlight and asks the other if they should bring it along. “Not necessary” is the reply. “We will be home before dark and it’ll just weigh you down.” The hiker examines the flashlight, holds it briefly to get a sense of its weight and throws it in the backpack. “Sure, it adds some weight”, he thinks, “but let’s carry it with us just in case.” Changing this one variable in the story changes the conclusion drastically. In this version the hikers still wait out the storm at the summit, but are then able to use the flashlight to negotiate the ledge in the dark and then make their way down the mountain. When they arrive safely at their car they are shaken by their experience and they are bitterly cold as the temperature has dropped during their descent. They also realize that adding the extra weight of the flashlight may have saved their lives.

Our goal is to compound shareholder capital over a full market cycle by participating sensibly when markets move up and striving to lose less when markets pull back. We continue to remain patient, stay prepared, and stick dilligently to our investment process.

Portfolio Overview

Buys and Sells

We added four new positions during the quarter. Newscorp (1.54% of Fund assets as of quarter end) and Jones Lang LaSalle, Inc. (1.09% of Fund assets as of quarter end) were added early in the quarter. Trisura Group Ltd (0.01% of Fund assets as of quarter end) was a spin-off of Brookfield Asset Management (4.77% of Fund assets as of quarter end). We also initiated a position in Conduent, Inc. (0.98% of Fund assets as of quarter end) late in the quarter.

We exited one position during the quarter: Philip Morris International, Inc. which we originally purchased in November 2013.

Cash

The Fund’s cash position (cash and cash equivalents) on June 30, 2017 was 32.41%, slightly higher than where we ended the prior quarter.

Risk and Volatility

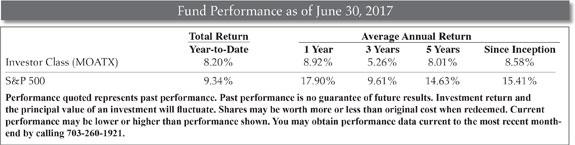

We define risk as the permanent loss of capital. We do not believe that volatility and risk are the same thing. While low volatility is not our goal, it has nonetheless been an outcome of our conservative approach to capital appreciation. For the five years ending June 30, 2017, the Fund’s beta was 0.54, roughly half that of the S&P 500. For the same period, our standard deviation was 6.30% versus a S&P 500 standard deviation of 9.56%. Up Capture versus the S&P 500 for the five year period was 56.58% and down capture was 57.96%.

Regards,

![]()

Caeli Andrews

Managing Director

Castle Investment Management

![]()

Andrew Welle

Managing Director

Castle Investment Management

The opinions expressed are those of the Fund’s Adviser and are not a recommendation for the purchase or sale of any security.

The Standard & Poors 500 Index (S&P 500) is an index of 500 stocks. Beta is a measure of the Fund’s sensitivity to a benchmark or broad market index which has a beta of 1.00. Standard deviation is used to measure an investment’s historic volatility. The up capture and down capture ratios are statistical measures of a manager’s overall performance in upward moving and downward moving markets, respectively. We define a full-market cycle as a period of time, usually measured in years, that includes both ‘bearish’ markets (the market trends down) and ‘bullish’ markets (the market trends up).

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The Prospectus contains this and other important information about the Fund, and it may be obtained by calling 1-877-743-7820, or visiting www.castleim.com. Read it carefully before investing.

The expense ratio excluding acquired fund expenses for the Investor Share Class is 1.34% (2.34% for Class C). The expense ratio including acquired fund expenses for the Investor Share Class is 1.36% (2.36% for Class C). Effective November 1, 2016 the Adviser has contractually agreed to waive Services Agreement fees by 0.24% of its average daily net assets through October 31, 2017. The Services Agreement fee waiver will automatically terminate on October 31, 2017 unless it is renewed by the Adviser. The Adviser may not terminate the fee waiver before October 31, 2017. The total expense ratio excluding the Services Agreement fee waiver for the Investor Share Class is 1.60% (2.60% for Class C). If you redeem Class C Shares of the Fund (for purchases made before November 1, 2016), your redemption may be subject to a 1.00% Contingent Deferred Sale Charge if the shares are redeemed less than one year after the original purchase of the Class C Shares.

The risks associated with the Fund, detailed in the Prospectus, include the risks of investing in small and medium sized companies and foreign securities which may result in additional risks such as the possibility of greater price volatility and reduced liquidity, different financial and accounting standards, fluctuations in currency exchange rates, and political, diplomatic and economic conditions as well as regulatory requirements in foreign countries. There also may be risks associated with the Fund’s investments in exchange traded funds, real estate investment trusts (“REITs”), significant investment in a specific sector, and nondiversification. Technology companies held in the Fund are subject to rapid industry changes and the risk of obsolescence. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

Distributed by Rafferty Capital Markets, LLC-Garden City, NY 11530.

Comments are closed.