Market Comments

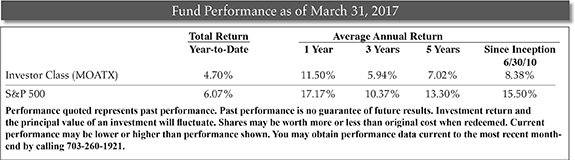

The beta for the Castle Focus Fund (MOATX) for the last five years is 0.55 versus the S&P 500. We start our quarterly commentary with this fact to remind our shareholders that we approach our objective of capital appreciation with a focus on striving to dampen drawdowns. In short, we look down before we look up. An important facet of this is that our goal is not to produce a low or attractive beta, but rather a low beta has been an outcome of our conservative approach to value investing. We believe that consistently applying this approach gives us the best chance of outperforming the benchmark over a full market cycle.

“Story stocks” have been driving the market for some time and this past quarter was no different. In our view, almost all story stocks are momentum-based and essentially driven by the crowd’s hunger for oversized gains. Investopedia defines a ‘story stock’ as “a stock whose value reflects expected future potential (or favorable press coverage) rather than its assets and income”. Momentum and emotion have been key drivers of many story stocks including the initial public offering of SNAP, Tesla’s market cap exceeding that of General Motors, or Amazon’s anticipated takeover of the entire retail sector. There is an excitement, a rush, to own the shiny new thing and, more importantly, to not miss out. And as the shares of a public company are finite, the fear of missing out can build momentum and the stock price can take on a life of its own. When story stocks are hot, it seems as if the party won’t and can’t stop.

In contrast, as fundamental value investors, story stocks do not fit our investment criteria. The investments we find attractive are often overlooked by mainstream media pundits and are not the subject of cocktail party conversations. We invest in fundamentally strong companies with uncomplicated business models and management teams that are executing on a long-term plan. We invest in these businesses when we can buy them at a significant discount to our estimate of their intrinsic value. We believe a portfolio of these types of businesses can outperform the broad market over a full-market cycle while also being less volatile and dampening drawdowns.

“Price is what you pay, value is what you get.” We practice this ‘Buffettism’ when managing the Castle Focus Fund by acquiring shares of valuable businesses when those shares are ‘marked down’. This past quarter the market continued to march higher which makes it more difficult to find ‘obvious bargains’. We continue to diligently follow our process and remain patient and disciplined. Our mindset in this long-lived bull market is summarized by another Warren Buffett quote: “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Portfolio Overview

Buys and Sells

We added two new positions during the quarter. Cameco Corp. (1.02% of Fund assets as of quarter end) was added late in the quarter. We re-initiated a position in CVS Heatlh Corp. (4.85% of Fund assets as of quarter end) which the Fund has previously owned from 2011 to 2014.

We exited four positions during the quarter: AmerisourceBergen Corp. which we originally purchased in October 2016; Emerson Electric Co. which we originally purchased in June 2016; Express Scripts Holding Co. which we had owned since October of 2013; and finally Franco-Nevada Corp. which we originally purchased in March of 2013.

Cash

The Fund’s cash position (cash and cash equivalents) on March 31, 2017 was 31.98%, slightly higher than where we ended the prior quarter.

Risk and Volatility

We define risk as the permanent loss of capital. We do not believe that volatility and risk are the same thing. While low volatility is not our goal, it has nonetheless been an outcome of our conservative approach to capital appreciation. For the five years ending March 31, 2017, the Fund’s beta was 0.55, roughly half that of the S&P 500. For the same period, our standard deviation was 6.74% versus a S&P 500 standard deviation of 10.20%. Up Capture versus the S&P 500 for the five year period was 56.18% and down capture was 59.86%.

As always, thank you for your investments in the Castle Focus Fund.

Kind Regards,

![]()

Caeli Andrews

Co-Founder, Managing Director

Castle Investment Management

![]()

Andrew Welle

Co-Founder, Managing Director

Castle Investment Management

The opinions expressed are those of the Fund’s Adviser and are not a recommendation for the purchase or sale of any security.

The Fund does not own shares of Snap, Inc., Tesla, Inc., General Motors Co., or Amazon.com, Inc.

The Standard & Poors 500 Index (S&P 500) is an index of 500 stocks. Beta is a measure of the Fund’s sensitivity to a benchmark or broad market index which has a beta of 1.00. Standard deviation is used to measure an investment’s historic volatility. The up capture and down capture ratios are statistical measures of a manager’s overall performance in upward moving and downward moving markets, respectively.

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The Prospectus contains this and other important information about the Fund, and it may be obtained by calling 1-877-743-7820, or visiting www.castleim.com. Read it carefully before investing.

The expense ratio excluding acquired fund expenses for the Investor Share Class is 1.34% (2.34% for Class C). The expense ratio including acquired fund expenses for the Investor Share Class is 1.36% (2.36% for Class C). Effective November 1, 2016 the Adviser has contractually agreed to waive Services Agreement fees by 0.24% of its average daily net assets through October 31, 2017. The Services Agreement fee waiver will automatically terminate on October 31, 2017 unless it is renewed by the Adviser. The Adviser may not terminate the fee waiver before October 31, 2017. The total expense ratio excluding the Services Agreement fee waiver for the Investor Share Class is 1.60% (2.60% for Class C). If you redeem Class C Shares of the Fund (for purchases

made before November 1, 2016), your redemption may be subject to a 1.00% Contingent Deferred Sale Charge if the shares are redeemed less than one year after the original purchase of the Class C Shares.

The risks associated with the Fund, detailed in the Prospectus, include the risks of investing in small and medium sized companies and foreign securities which may result in additional risks such as the possibility of greater price volatility and reduced liquidity, different financial and accounting standards, fluctuations in currency exchange rates, and political, diplomatic and economic conditions as well as regulatory requirements in foreign countries. There also may be risks associated with the Fund’s investments in exchange traded funds, real estate investment trusts (“REITs”), significant investment in a specific sector, and nondiversification. Technology companies held in the Fund are subject to rapid industry changes and the risk of obsolescence. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

Distributed by Rafferty Capital Markets, LLC-Garden City, NY 11530.

Comments are closed.