Market Comments

Do kids today even know what a ‘broken record’ sounds like? Now that nearly all music is on our phones and other devices, we’re fairly sure that a skipping record is as foreign to digitally-raised youngsters as cassette decks, phone booths, and typewriters. We are familiar enough with the colloquialism to remind you to place a penny on the record player stylus head to avoid the skipping.

Many things about today’s market remind us of a skipping record.

To download a PDF of this report, click here.

First, markets seem to be stuck in a groove of small upward moves. The S&P 500 has produced positive returns for each of the first nine months in 2017. Additionally, the index has moved up for 11 consecutive months without experiencing a monthly loss. Looking back further, the S&P 500 has produced positive returns in 20 of the last 24 months. How many months in a row the index has advanced is of very little concern to us. As value investors we care about the fundamentals of the companies that we own or are interested in owning and the price that we pay for those companies. This is the standard by which we test our investment process: Do the companies that we currently own trade at a discount to our conservative estimate of their fair value and do the fundamentals of each company equate to ‘quality’ in our opinion? We want to participate sensibly in upward moving markets and we want to limit the effects of market downdrafts. Thus our approach requires patience – and a willingness to diverge from the benchmark – as we allocate shareholder capital when purchases can be made at a significant discount to our conservative estimate of fair value.

Second, it feels to us as if market pundits continuously make the same noise day in and day out: FANG stocks, the drama at Uber, and bitcoin seemingly dominate the coverage at CNBC.1 As an example of this, we recall a recent day in September when FANG stocks unexpectedly didn’t advance, but instead were down steeply. That day we watched a CNBC segment that didn’t address the fundamentals and ask why those stocks were experiencing losses, but instead wondered what was the next best group of stocks to put your money in. Our process is long-term oriented and does not waver regardless of market sentiment. We are not looking for the next best group of stocks to invest in. Rather we are looking for the best individual companies to invest in at the right price.

Finally, we admit that our message may sound like a broken record, which is par for the course for value investors. We are reminded of Boston-based GMO in the late 1990’s who adhered to their value approach while internet and technology stocks surged. Critics said they had lost their touch and did not recognize the transformative power of the ‘new economy’. Shareholders left in droves. We understand that value investing can be lonely at times. Renowned value investor Jean-Marie Eveillard said “It’s warmer inside the herd. It can be very cold outside of it.” As you have heard us say many times before, our investment process is to purchase a stock when it can be bought at a significant discount to our conservative estimate of its intrinsic value. We run a concentrated portfolio so we don’t need to find hundreds of companies, just 15 to 30 companies that meet our criteria. In the absence of these obvious bargains, we will wait patiently for attractive entry points.

Portfolio Overview

Buys and Sells

We added Loews Corporation (L, 2.01% of Fund assets as of 9/30/17) to the Fund during the third quarter of 2017. We believe that Loews’ respective portfolio components are well positioned to create additional shareholder value. Loews’ strong balance sheet could provide downside support for the company’s shares as well as a valuable resource to capitalize on opportunistic mergers or acquisitions as they present themselves. We have an estimate of intrinsic value for Loews at approximately $77 per share. At quarter end the stock closed at $47.86.

Cash

The Fund’s cash position (cash and cash equivalents) on September 30, 2017 was 34.53%, slightly higher than where we ended the prior quarter.

Risk and Volatility

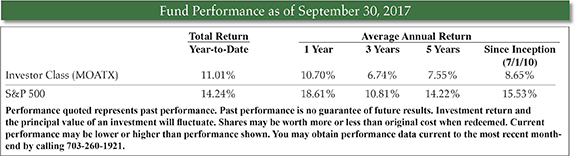

We define risk as the permanent loss of capital. We do not believe that volatility and risk are the same thing. While low volatility is not our goal, it has nonetheless been an outcome of our conservative approach to capital appreciation. For the five years ending September 30, 2017, the Fund’s beta was 0.53, roughly half that of the S&P 500. For the same period, our standard deviation was 6.26% versus a S&P 500 standard deviation of 9.55%. Up Capture versus the S&P 500 for the five year period was 55.49% and down capture was 57.96%.

Regards,

![]()

Caeli Andrews

Managing Director

Castle Investment Management

![]()

Andrew Welle

Managing Director

Castle Investment Management

The opinions expressed are those of the Fund’s Adviser and are not a recommendation for the purchase or sale of any security.

The Standard & Poors 500 Index (S&P 500) is an index of 500 stocks. Beta is a measure of the Fund’s sensitivity to a benchmark or broad market index which has a beta of 1.00. Standard deviation is used to measure an investment’s historic volatility. The up capture and down capture ratios are statistical measures of a manager’s overall performance in upward moving and downward moving markets, respectively. We define a full-market cycle as a period of time, usually measured in years, that includes both ‘bearish’ markets (the market trends down) and ‘bullish’ markets (the market trends up).

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The Prospectus contains this and other important information about the Fund, and it may be obtained by calling 1-877-743-7820, or visiting www.castleim.com. Read it carefully before investing.

The expense ratio excluding acquired fund expenses for the Investor Share Class is 1.34% (2.34% for Class C). The expense ratio including acquired fund expenses for the Investor Share Class is 1.36% (2.36% for Class C). Effective November 1, 2016 the Adviser has contractually agreed to waive Services Agreement fees by 0.24% of its average daily net assets through October 31, 2017. The Services Agreement fee waiver will automatically terminate on October 31, 2017 unless it is renewed by the Adviser. The Adviser may not terminate the fee waiver before October 31, 2017. The total expense ratio excluding the Services Agreement fee waiver for the Investor Share Class is 1.60% (2.60% for Class C). If you redeem Class C Shares of the Fund (for purchases made before November 1, 2016), your redemption may be subject to a 1.00% Contingent Deferred Sale Charge if the shares are redeemed less than one year after the original purchase of the Class C Shares.

The risks associated with the Fund, detailed in the Prospectus, include the risks of investing in small and medium sized companies and foreign securities which may result in additional risks such as the possibility of greater price volatility and reduced liquidity, different financial and accounting standards, fluctuations in currency exchange rates, and political, diplomatic and economic conditions as well as regulatory requirements in foreign countries. There also may be risks associated with the Fund’s investments in exchange traded funds, real estate investment trusts (“REITs”), significant investment in a specific sector, and nondiversification. Technology companies held in the Fund are subject to rapid industry changes and the risk of obsolescence. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

Distributed by Rafferty Capital Markets, LLC-Garden City, NY 11530.